GROWTH RATE SLOWS BUT TRAFFIC STILL RISING AT EUROPE’S AIRPORTS

Share

ACI Europe today revealed that passenger traffic continued its upward trajectory across the continent’s airports in the first half of 2019, rising 4.3% despite a “range of economic, geopolitical and industry specific challenges”.

The rate of growth has slowed, however, compared to the same period in 2018 and ACI Europe believes air transport in Europe faces an uncertain outlook going forward.

Air cargo continues to disappoint, declining by 3.5% in the first six months of 2019.

ACI Europe director general, Olivier Jankovec, says: “Passenger traffic growth has certainly slowed this year compared to previous ones, but it still remains quite resilient – especially given the range of economic, geopolitical and other industry-specific challenges we are confronted with.

“Slowing economic growth in Europe, trade wars and Brexit are not helping – and neither are rising fuel bills, ATM disruptions, airline consolidation and aircraft grounding and delivery delays.

“Aircraft movements have been continuously slowing down – from +6.2% last December to just +1.6% in June. This shows just how risk averse airlines have become in terms of capacity deployment & network development.”

He adds: “The slump in freight traffic is where it really bites at the moment. And it is not getting any better, with June registering a drop of -7.1% – the worst monthly performance in more than seven years.

“This does not bode well for the months ahead, especially as passenger traffic usually does not remain totally isolated from trends in freight traffic.”

The EU market maintained steady growth during H1, with passenger traffic performance holding steady between 4.5% to 5% on a month-by-month basis over the period.

Airports in Austria (+20%), Croatia (+10.5%) and Estonia (+10.5%) posted double-digit growth in H1, with those on Luxembourg, Portugal, Spain, Latvia, Poland, Hungary and Romania also growing well above the EU average.

Conversely, Bulgaria (-2.5%) and Sweden (-4.1%) reported passenger traffic declining while growth was flat in neighbouring Denmark (+0.3%).

Belgium, the Netherlands, Slovenia and the UK significantly underperformed the EU average – with the latter further slowing down in June (+0.9%).

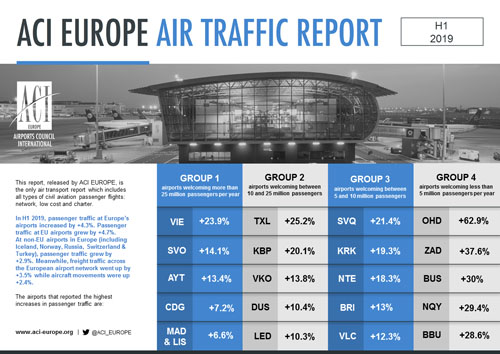

Accordingly, amongst larger/capital EU airports, the best results were achieved by Berlin TXL (+25.2%), Vienna (+23.9%), Tallinn (+10.5%), Dusseldorf (+10.4%), Milan Malpensa (+10.2%), London Luton (+9.6%), Riga (+9.5%) Luxembourg (+9.0%), Bucharest Otopeni (+8.2%), London City (+7.8%), Athens (+7.7%), Budapest (+7.5%) and Warsaw (+7.4%).

Airports in the non-EU market grew at a slower pace in H1, mainly due to traffic losses in Turkey (-1.4% – as a result of the recession affecting the country) and Iceland (-20.3% – following the bankruptcy of WOW in the final days of March) as well as nearly flat growth in Norway (+0.9%).

However, passenger traffic in Ukraine, Georgia, Albania and Northern Macedonia remained extremely dynamic, achieving double-digit growth.

It is also worth noting that passenger traffic in Turkey improved in Q2 and ended up posting an impressive +7.1% growth in June – signaling a recovery.

The best performances amongst larger/capital non-EU airports came fromKyiv-Boryspil(+20.1%), Moscow-Sheremetevo (+14.1%), Moscow-Vnukovo (+13.8%), Antalya (+13.4%), Pristina (+12.5%), Tbilisi (+11.7%), Tirana (+11.1%), and Saint Petersburg (+10.3%).

{kind=link}